Which payment methods are relevant for B2B transactions?

After we looked into the functioning of B2B payments, we continue our series with a deep dive on payment methods and which of them are most relevant for performing B2B transactions.

Before we start, we want to put a couple of disclaimers for this article, because a lot of lists tend to mix payment methods with payment goals. The most prominent example of this would be payment by invoice which is used synonymously with a transaction that offers a specific payment goal of for example 14, 30, 90 days. Technically speaking, a payment by invoice is always a bank transfer and not a standalone payment method while no matter which payment method you choose, you will always get an invoice with it. This dynamic just shows us, that in contrast to the B2C market, B2B transactions are aways a function of a payment method and a specific payment goal.

Flexible payment goals are essential in B2B transactions to accommodate industry standards - that's why we will split up the analysis into two parts. Part one (this article) will strictly focus on payment methods while part two will take a look at different payment goals and financing options.

Bank Transfers:

Bank transfers are still the most used channel when it comes to B2B transactions. Their functioning is similar to consumer transactions, just under a business context, meaning transactions can happen between companies operating in the same country or different countries - and transactions happen with a usual delay of 2-3 bank days or even instantly. Their cost effective nature especially for smaller sums and national transfers makes them very attractive in their application. Costs range usually between 0.00€ - 5,00€ and rarely even surpass 10,00€ - except for big and international transactions.

Although bank transfers rely on electronic systems for processing the payment, they require some manual steps in order to initiate or verify transactions. Companies usually deploy whole departments or specific employees who handle the transfers out of the respective accounts which can lead to complex processes resulting in missed, late and wrong payments from the initiator.

Bank transfers are especially used under the context of pre-payment, escrow-connected processes (e.g. car payments) and payment by invoice. For all of these transaction types usually the seller issues an invoice or transaction instruction with their bank details and the buyer initiates a transfer from his account.

Advantages:

- Cost-effective

Disadvantages:

- Inconvenience for buyers

- Increased manual efforts for seller (reconciliation)

- High proneness for human errors

- Buyer default risk (for invoice payments)

Most used application:

- Pre-Payments

- Invoice payments

- Escrow-like payments

- Large transactions

- International transactions

Bank Debits:

Bank debits, also known as direct debits in the European Area, allow businesses to collect payments directly from customers' bank accounts - usually through a (digital) form asking for permission. For businesses, bank debits provide a reliable and automated way to receive payments as they are by nature pull payments, meaning the recipient has full control over the transaction. Once authorized by the customer, the business can initiate transactions to collect funds directly from the customers' bank accounts on agreed-upon dates, eliminating the need for manual invoicing and payment reconciliation. Direct debits are commonly used in subscription payments like insurances and less for bigger one time transactions since their regulatory setup allow the payer to revoke the payment for up to 8 weeks after execution.

Advantages:

- Cost-effective

- Super convenient for buyers and sellers

- Low internal efforts for seller (reconciliation)

Disadvantages:

- Default risk

- Regulatory setup allows for a long revoking period

Most used application:

- Subscription like payments

- Transactions between known partners

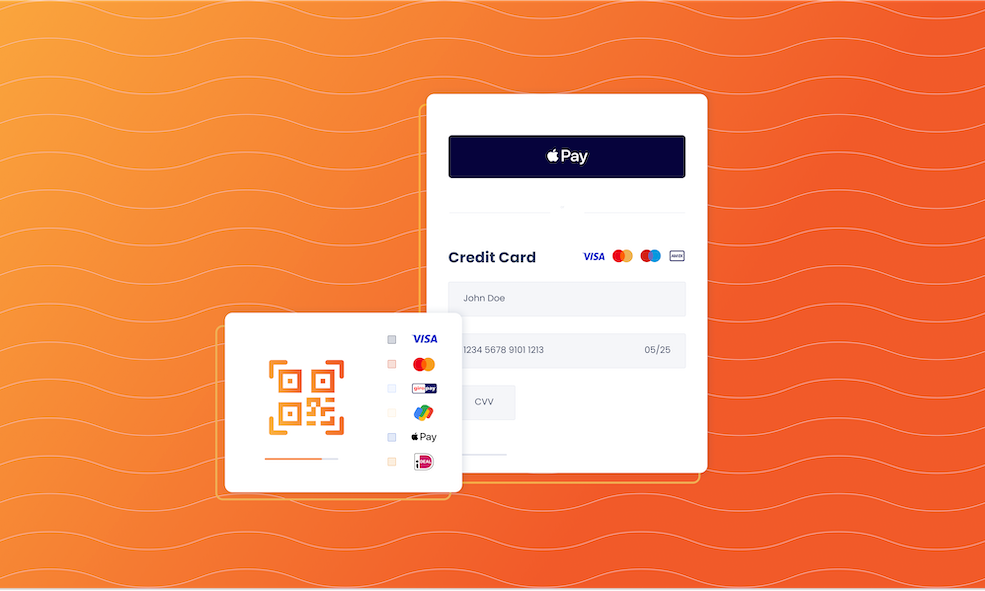

Credit Cards / Wallets:

Credit cards and wallets are are widely used payment methods in the B2C industry but their application is still less common in the B2B world. The main reason for that is costs as credit cards and payment providers are usually charging up to 2% for a transaction which especially for high value baskets (eg. bulk orders, machines) can take a lot from the companies margin. Nevertheless, cards and wallets have seen a rise in their application in recent years due to the platformization of procurement - especially for smaller and uprising companies. This lead to the effect that on platforms like Alibaba, Temu or Ankorstore, credit cards are highly used payment methods as they provide the advantage of an internationally unified UX and security of transaction.

Thus paying with a credit card on B2B marketplaces and platforms is one of the easiest payment options. Your buyers need to type in their card number, its expiration date, and the three-digit security code at the back (CCV) during checkout. At this point, the buyer might be redirected to their credit card issuer's online portal for an additional layer of security. This is where the buyer may need to enter an authentication code or provide other verification, depending on the card's security measures. All of this information is securely transmitted to the payment processor, which verifies the details and completes the transaction. This way, your buyers can shop and pay quickly with only a few steps. It's great for smaller to medium-sized purchases and gives businesses some extra time and flexibility to manage their money.

Advantages:

- Practically risk-free

- Super convenient for buyers

- Low internal efforts for seller (reconciliation)

- Internationally standardized and recognized

Disadvantages:

- Expensive

- Business transaction are not regulated from pricing perspective

Most used application:

- Smaller transactions

- International transactions